It was reported recently that Shell, the oil giant, had bought a company, New Motion, a Dutch firm with 30,000 private charging points at home and offices in Europe. This is an interesting development, and it indicates that the oil giants are contemplating a business life after oil.

Profitable business selling petrol

The downstream sector, especially the retailing of petroleum products such as gasoline (petrol) and diesel, contributes a major proportion of the oil giants’ revenue. A small developing country like Malaysia has a large petroleum products retail market. The local oil giants such as Petronas, Petron and Shell enjoyed billions of RM from sales of petroleum products. The size of the petroleum products market was worth more than RM60 billion in 2014, based on the annual reports of the three companies. If sales of other smaller players like BP Petroleum and Caltex are included, the total market would be more than RM65 billion.

According to Petroleum Dealers Association of Malaysia, there are more than 3,500 petrol stations in Malaysia. As petroleum products such as gasoline and diesel are volatile and are subject to stringent safety requirements, dedicated petrol outlets are required. The first modern petrol station was established in 1913 in US.

Over the years, petrol stations have added products such as foods and drinks, and some bigger petrol stations have attached fast-food restaurants. The sales of petroleum products still make up the biggest proportion of sales of the oil giants, which result in enormous profit for them.

The Expected Withering of the Petrol Stations

The entry of Shell into the electric car charging business shows that the oil giants are facing a major disruption to its retailing of petroleum products business sector. These petrol stations have made the oil giants into well-known brands and corporate power.

The electric car revolution would have a major impact on the long-term viability of the petrol stations as a business. Electric cars will be embraced by consumers, first in the developed countries, followed by developing countries. Car manufacturers and other companies are racing each other to develop electric cars with longer range. Many countries such as Netherlands are encouraging cities and electricity generating companies to install charging stations at housing estates, homes, hypermarkets car parks and elsewhere.

Impact of the Oil Giants’ Revenue in Malaysia

Although the penetration of electric cars in Malaysia is still small, the Malaysian government is committed by international treaties to reduce toxic emission from fossil fuels. In addition, the price of electric cars will continue to decline as innovative companies such as Tesla and Nissan are developing denser batteries at cheaper prices.

Electric car being charged

The adoption of electric cars in Malaysia will be patchy initially. We foresee tax incentives may spur consumers to purchase electric cars due to various reasons, such as convenience of recharging and advanced features of electric cars such as self-driving. We foresee there would be no turning back to the adoption of electric cars in Malaysia.

The impact to the oil giants’ revenue would also be significant. At the market worth of petroleum products of more than RM65 billion per annum, a tenth reduction of consumption of petrol would amount to RM6.5 billion of lost revenue per year. The amount of lost revenue would be serious with higher adoption of electric cars. Tax revenue to the Malaysian government will also reduce as tax forms a major component of the price of petrol.

Shell believes that consumers will patronize its petrol stations to charge their electric cars. Currently, consumers have no choice but to go to petrol stations to fill-up petrol into their cars.

We expect that charging stations will be available in all sorts of locations as long as there is supply of electricity. Why should consumers go to a Shell petrol station to charge their electric cars when they can do it at homes?

Could we see the slow death of the ubiquitous petrol stations with the large logos of the oil giants standing high and can be seen from far?

A report by Oxford Martin School, University of Oxford (The Report), has examined the susceptibility of jobs to computerization. The impact of computerisation on jobs (labour market) is well-established. It is documented that there will be a decline in routine -intensive occupations, that is, occupations mainly consisting of task following well-defined procedures that can easily be performed by sophisticated algorithms.

At the same time, with falling prices of computers, problem-solving skills are becoming productive, which explains substantial employment growth in occupations involving cognitive tasks where skilled labour has a comparative advantage. According to Brynjolfsson and McAfee (2011), technological innovation is still increasing with more sophisticated technologies disrupting labour by making workers and employees redundant.

According to Autor, et al. (2003) workplace tasks can be categorized as follows:

Routine versus non-routines tasks, and

Manual versus cognitive tasks.

In short, routine tasks are defined as tasks that follow explicit rules that can be accomplished by machines while, while non-routine tasks are not sufficiently well understood in computer codes. Each of these task categories can, in turn, be of either manual or cognitive in nature, that is, they relate to physical labour or knowledge work.

Perception and Manipulation Tasks

Robots are still unable to match the depth and breadth of human perception. While basic geometric identification is reasonably mature, enabled by the rapid development of sophisticated sensors and lasers, significant challenges remain for more complex perception tasks, such as identifying objects and their properties in a cluttered field of view. As such, tasks that relate to an unstructured work environment can make jobs less susceptible to computerisation. The difficulty of perception has ramifications for manipulation tasks. This is, in particular, the handling of irregular objects, for which robots are yet to reach human level of aptitude.

A related challenge is failure recovery, that is, identifying and rectifying the mistakes of the robot when it has, for example, dropped an object. Manipulation is also limited by the difficulties of planning out the sequence of actions required to move an object form one place to another.

The main challenges to robotic computerization, perception and manipulation, thus largely remain and are unlikely to be fully resolved in the next decade or two.

Prone to computerization

Creative and Intelligence Tasks

The psychological processes underlying human creativity are difficult to specify. According to Borden (2003), creativity is the ability to come up with ideas or artifacts that are novel and valuable. Ideas, in a broader sense, include concepts, poems, musical compositions, scientific theories, cooking recipes and jokes, whereas artifacts are objects such as paintings, sculptures, machinery and pottery. One process of creating ideas (and similarly artifacts) involves making unfamiliar combinations of familiar ideas, requiring a rich store of knowledge. The challenge here is to find some reliable means of arriving at combinations that “make sense.”

It seems unlikely that occupations requiring a high degree of creative intelligence will be automated in the next decades.

Social Intelligence Tasks

Human social intelligence is important in a wide range of work tasks, such as those involving negotiations, persuasion and care. While algorithms and robots can reproduce some aspects of human social interaction, the real-time recognition of natural human emotion remains a challenging problem, and the ability to respond intelligently to such inputs is even more difficult. Even simplified versions of typical social tasks prove difficult for computers, as is the case in which social interaction is reduced to pure text.

The authors of the Oxford Martin School’s report noted that while sophisticated algorithms and development in MR, building upon big data now allow many non-routine tasks to be automated, occupations that involve complex perception and manipulation tasks, creative intelligence tasks, and social intelligence tasks are unlikely to be substituted by computer capital over the next decades or two.

The probability of an occupation being automated can thus be described as a function of these task characteristics.

Measuring Impact of Computerisation

The Report, using 702 detailed occupation information of the US Labour Department’s Standard Occupation Classification (SOC), has developed a model to measure the impact of computerization of various types of occupations.

Table 1 shows the top 20 occupations that are least-computerisable , while Table 2 shows the top 20 occupations that are most-computerisable.

Table 1: Top 20 Least-Computerisable

Rank

Probability

SOC Code

Occupation

1

0.0028

29-1125

Recreational Therapists

2

0.003

49-1011

First-Line Supervisors of Mechanics, Installers and Repairers

3

0.003

11-9161

Emergency Management Directors

4

0.0031

21-1023

Mental Health and Substance Abuse Social Workers

5

0.0033

29-1181

Audiologists

6

0.0035

29-1122

Occupational Therapists

7

0.0035

29-2091

Orthotists and Prosthetists

8

0.0035

21-1022

Healthcare Social Workers

9

0.0036

29-1022

Oral and Maxillofacial Surgeons

10

0.0036

33-1011

First-Line Supervisors of Fire Fighting and Prevention Workers

11

0.0039

29-2031

Dietitians and Nutritionists

12

0.0039

11-9081

Lodging Managers

13

0.004

27-2032

Choreographers

14

0.0041

41-9031

Sales Engineers

15

0.0042

29-1060

Physicians and Surgeons

16

0.0042

25-9031

Instructional Coordinators

17

0.0043

19-3039

Psychologists and, All Others

18

0.0044

33-1012

First-Line Supervisors of Police and Detectives

19

0.0044

29-1021

Dentists, General

20

0.0044

25-2021

Elementary School Teachers

Table 2: Top 20 Most-Computerisable

Rank

Probability

SOC Code

Occupation

1

0.99

41-9041

Telemarketers

2

0.99

23-2093

Title Examiners, Abstractors and Searchers

3

0.99

51-6051

Sewers Hand

4

0.99

15-2091

Mathematical Technicians

5

0.99

13-2053

Insurance Underwriters

6

0.99

49-9064

Watch Repairers

7

0.99

43-5011

Cargo and Freight Agents

8

0.99

13-2082

Tax Preparers

9

0.99

51-9151

Photographic Process Workers

10

0.99

43-4141

New Account Clerks

11

0.99

25-4031

Library Technicians

12

0.99

43-9021

Data Entry Keyers

13

0.98

51-2093

Timing Device Assemblers and Adjusters

14

0.98

43-9041

Insurance Claims and Policy Processing Clerks

15

0.98

43-4011

Brokerage Clerks

16

0.98

43-4151

Order Clerks

17

0.98

13-2072

Loan Officers

18

0.98

27-2023

Umpires, Referees and Other Sport Officials

19

0.98

43-3071

Tellers

20

0.98

51-9194

Etchers and Engravers

Please see the whole list of 702 occupations in Appendix of Oxford Martin School’s Report.

Highlights

The Report’s main conclusions are as follows:

It distinguishes high, medium and low risk occupations, depending on their probability of computerisation. It makes no attempt to estimate the number of jobs that will actually be automated, and focus on potential job automatability over some unspecified number of years.

It predicts that most workers in transportation and logistics occupations, together with the bulk of office and administrative support workers, and labour in production occupations, are at risk.

It provides evidence that wages and educational attainment exhibit a strong negative relationship with the probability of computerization.

It implies that as technology races ahead, low-skill workers will reallocate to tasks that are non-susceptible to computerization, that is, tasks requiring creative and social intelligence. For workers to win the race, however, they will have to acquire creative and social skills.

Reference:

Carl Benedict Frey, and Micheal A. Osborne (20130, The future employment: How susceptible are jobs to computerisation. Working Paper, Oxford Martin School, University of Oxford.

Brynjolfsson and E. McAffe (2011). Race against the machine: How the digital revolution is accelerating innovation, driving productivity, and irreversibility transforming employment and economy. Digital Frontiers Press, Lexington, MA.

A. Boden (2003). The creative mind: Myths and mechanisms. Routledge.

Autor, F. Levy and R. J. Murnane (2003). The skill content of recent technological change: Am empirical exploration. The Quarterly Journal of Economics. Vol. 118, no.4, pp. 1279-1333.

The recent Frankfurt Motor Show in September 2917 saw major car companies exhibited several models of electric cars. Subsequently, investors are piling-up their bets on mining companies that are involved in lithium, the key component for making batteries for electric cars. BlackRock, one of the largest fund managers in the world, has emerged as a investor of lithium start-ups.

The BlackRock World Mining Trust, which has more than £800 million in assets and is co-managed by Evy Hambro, has become the largest shareholder in a handful of small mining companies aiming to produce lithium for use in batteries.

Demand for lithium has surged as the first mass market electric vehicles (EVs) such as the Tesla Model 3, Nissan Leaf and Chevrolet attract buyers. Growing demand for EVs has sparked a scramble to locate new supplies of lithium and prices have jumped about 26 per cent this year, making it one of the best performing commodities this year.

“Today the energy space is evolving towards a low carbon footprint and the combustion engine is going to be replaced with an alternative, “ Mr. Hambro said. “We want to be invested in companies that will be producing the raw materials that will be needed to meet this growth.”

Mr. Hambro is one of the world’s most influential mining investors, and his views are closely followed by the industry.

BlacRock’s investment parallels a growing investor interest in lithium as regulators push a transition to electric cars and battery costs continue to delcine. For example, assets in the Global X Lithium & Battery Tech exchange traded fund have quadrupled during this year from US$114 million to $484 million, while the Solactive Global Lithium index, made up of 26 miners and battery makers, had delivered a total return of 51 per cent this year.

Lithium production is currently dominated by four large firms, Chile’s SQM, FMC, Albermarle and Tianqi Lithium. A number of smaller companies are racing to bring supply to market and get their materials approved for use in batteries.

Over the past year around US$1.0 billion has been raised by lithium developers and explorers, but the funding will need to be increased to US$6.0 billion in 2025 to meet demand, according to Simon Moors of Benchmark Mineral Intelligence in London, which tracks lithium prices.

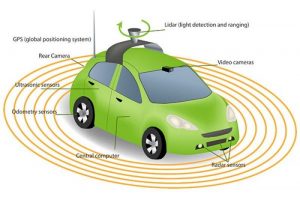

A Boon for Sensor Makers

Lithium producers are not only enjoying from electric car revolution. Sensor makers are also experiencing a boon. As electric cars become a reality, carmakers and their suppliers are confronting challenges that appeared less tangible when the dream of electric cars was a more distant vision.

A self-driving car of the future will be quipped with at least 20 sensors using cameras, radar and lidar to “see” its surroundings.

Some of the data must be transmitted to the “cloud” so the car cam communicate with its surrounding, but programming the software to send only the relevant data is a central challenge, says Elmar Degenhart, chief executive of the parts supplier Continental.

He says a self-driving car collects raw data at a rate of up to 15 gigabytes per second. By comparison, a person watching Netflix in high definition at home would consume three gigabytes of data per hour. “We need a different kind of electronic architecture to handle these volumes of gigabytes, “ he says.

The energy just required to power these self-driving systems is so great that a prototype electric car with a 400 km range can drive only 200 km autonomously, notes Scott Gallett, vice-president of marketing for BorgWarner, a maker of propulsion systems.

Sensors in an autonomous car

“One of the things people don’t talk about is just how much energy is really required by by the computers, the sensors, the radars, “he says. “Some of the prototypes out right now require just as much as energy as it does to propel the vehicle.”

Mr. Gallett believes that hybrid vehicles—often considered as a stop-gap measure to full electric cars— will experience a lengthier phase than many assume, because if autonomous technologies become popular then cars driven solely by batteries might not have enough energy to power bith the car and the computing system.

“Don’t think autonomous equals elecytric,” he adds.

Reference: FTWeekend 16 September/17 September 2017